This tutorial explores the ARIMA model for time series forecasting in Python, covering fundamentals, model building, and tuning with practical examples. It’s designed to help you effectively forecast and analyze trends in time series data.

ARIMA Model For Time Series

The steps which involved are shown below:

Step 1: Import Libraries

import pandas as pd import matplotlib.pyplot as plt from statsmodels.tsa.arima.model import ARIMA from statsmodels.tsa.stattools import adfuller

Step -2: Load the Dataset

# Load the data

df = pd.read_csv('/content/Task3.csv', parse_dates=['Date'], index_col='Date')

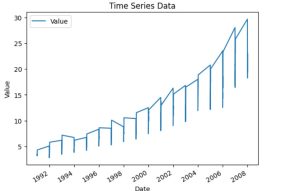

Step -3: Visualize the data

# Visualize the data df.plot(title='Time Series Data', ylabel='Value', xlabel='Date') plt.show()

“Time series data plot showing a rising trend, used in ARIMA model forecasting analysis.”

Step 4: Check for stationarity

# Define p, d, q values (initial guesses)

p = 1 # autoregressive part

d = 1 # differencing part (0 if the data is stationary)

q = 1 # moving average part

# Check for stationarity

result = adfuller(df['Value'])

print(f'ADF Statistic: {result[0]}')

print(f'p-value: {result[1]}')

ADF Statistic: 3.14518568930673 p-value: 1.0

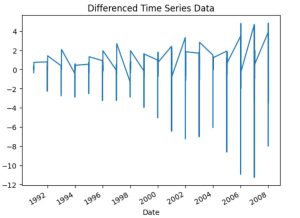

Step 5: If not stationary, apply differencing

# If not stationary, apply differencing

if result[1] > 0.05:

df['value_diff'] = df['Value'].diff().dropna()

df['value_diff'].plot(title='Differenced Time Series Data')

plt.show()

# Fit ARIMA model (after differencing)

model = ARIMA(df['value_diff'].dropna(), order=(p, d, q))

else:

# Fit ARIMA model (no differencing needed)

model = ARIMA(df['Value'], order=(p, d, q))

“Plot of differenced time series data showing fluctuations, used in ARIMA model preprocessing for trend removal and stationarity.”

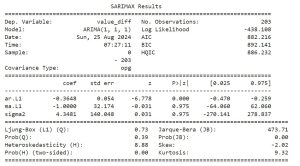

Step 6: Fit the model and Print Summary

# Fit the model model_fit = model.fit() # Print model summary print(model_fit.summary())

“ARIMA model summary output displaying key coefficients, standard errors, and statistical tests for time series forecasting analysis.”

Step 7: Plot diagnostics

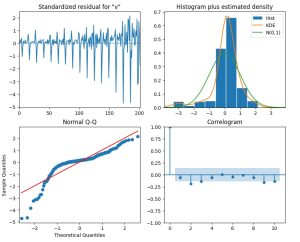

# Plot diagnostics model_fit.plot_diagnostics(figsize=(10, 8)) plt.show()

The image show a time series analysis plot, including standardized residuals, a histogram and density plot, a normal Q-Q plot, and a correlogram.

Step 8: Forecast future values

# Forecast future values forecast = model_fit.get_forecast(steps=10) forecast_df = forecast.conf_int() forecast_df['Forecast'] = model_fit.predict(start=forecast_df.index[0], end=forecast_df.index[-1]) forecast_df['Value'] = df['Value'][-1]

A 10-step prediction with confidence intervals is generated and compared against the actual data in a DataFrame.

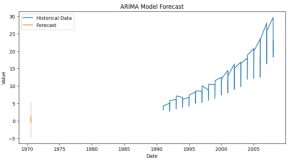

Step 9: Plot forecast

# Plot forecast

plt.figure(figsize=(10, 5))

plt.plot(df['Value'], label='Historical Data')

plt.plot(forecast_df['Forecast'], label='Forecast')

plt.fill_between(forecast_df.index, forecast_df.iloc[:, 0], forecast_df.iloc[:, 1], color='pink')

plt.legend(loc='upper left')

plt.title('ARIMA Model Forecast')

plt.xlabel('Date')

plt.ylabel('Value')

plt.show()